Commodity Dependence and Industrialization: The Economic Path of Latin America

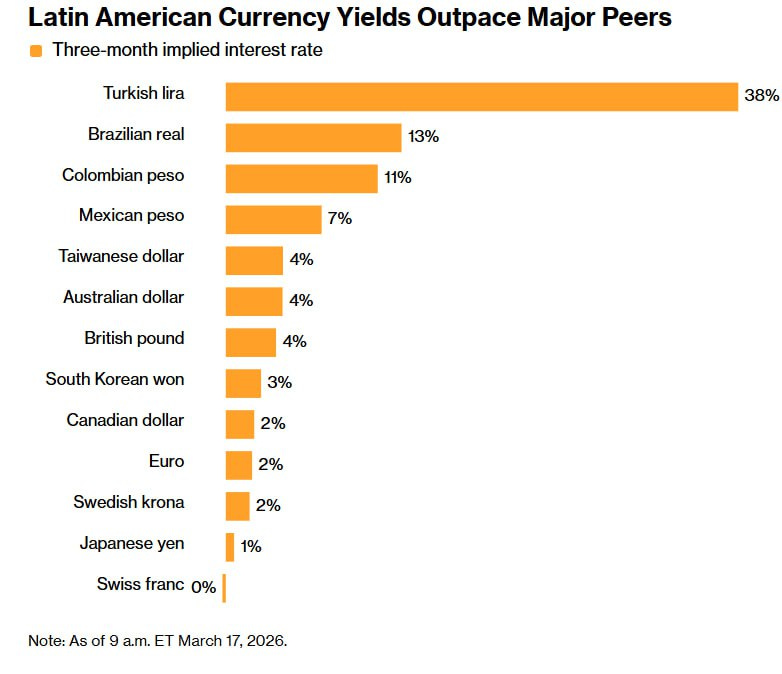

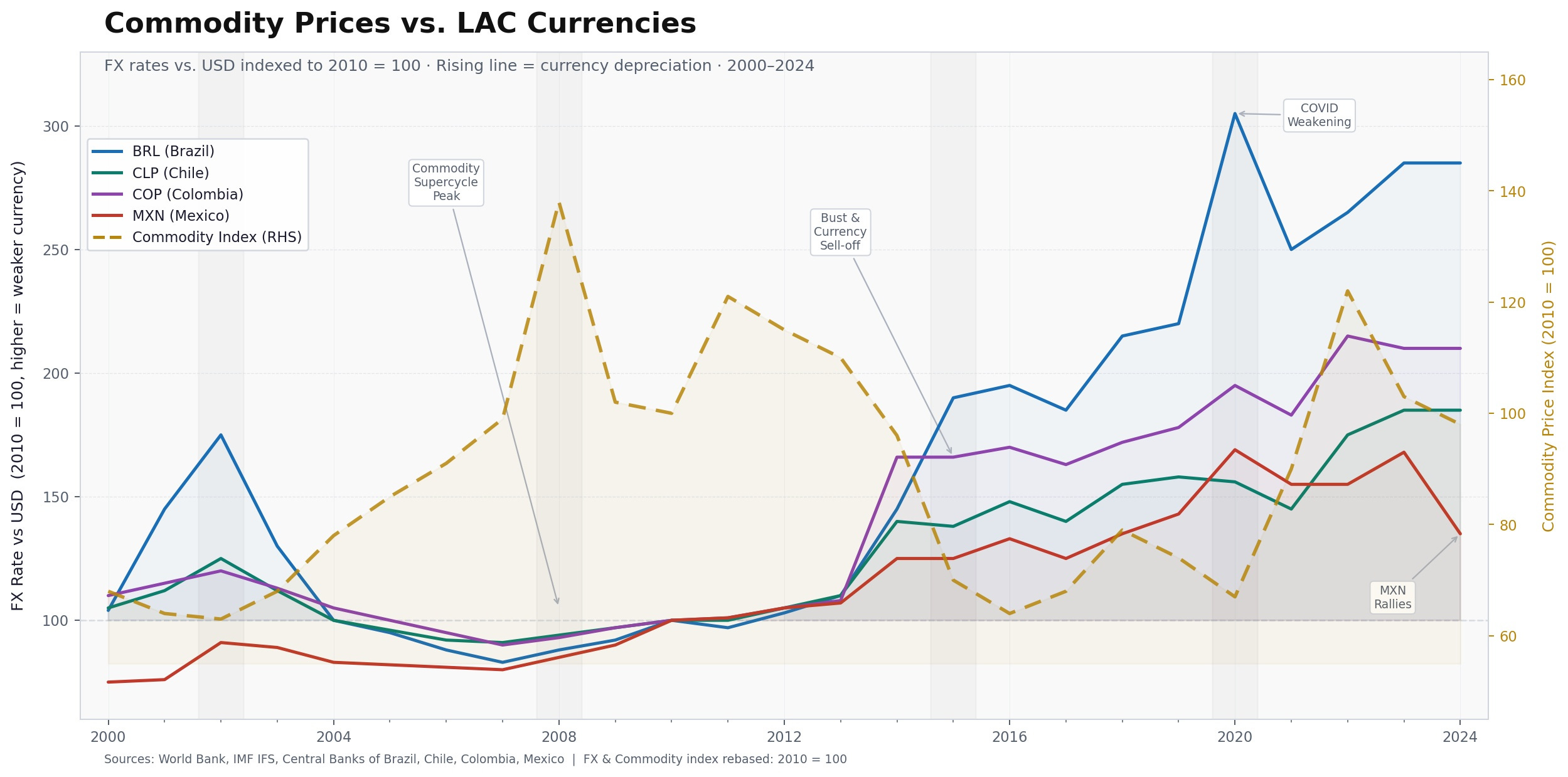

In March 2026, the global commodity markets have once again taken center stage. Rising geopolitical tensions, particularly in the Middle East, have pushed crude oil prices higher, triggering a familiar reaction across financial markets. Latin American currencies ,especially those of commodity exporting economies have strengthened even as commodities importers from Asia to europe has suffered higher depreciation. The Optimism in LATAM currencies is supported by improving terms of trade and relatively high interest rates. As reflected in FX markets, currencies such as the Brazilian real, Colombian peso, and Mexican peso have attracted capital flows, offering some of the highest yields globally.

At first glance, this appears to signal economic strength. Higher commodity prices improve export revenues, strengthen fiscal balances, and support currency appreciation. For global investors, Latin America once again looks attractive — a classic combination of carry and commodities.

Yet beneath this financial strength lies a more complex reality.

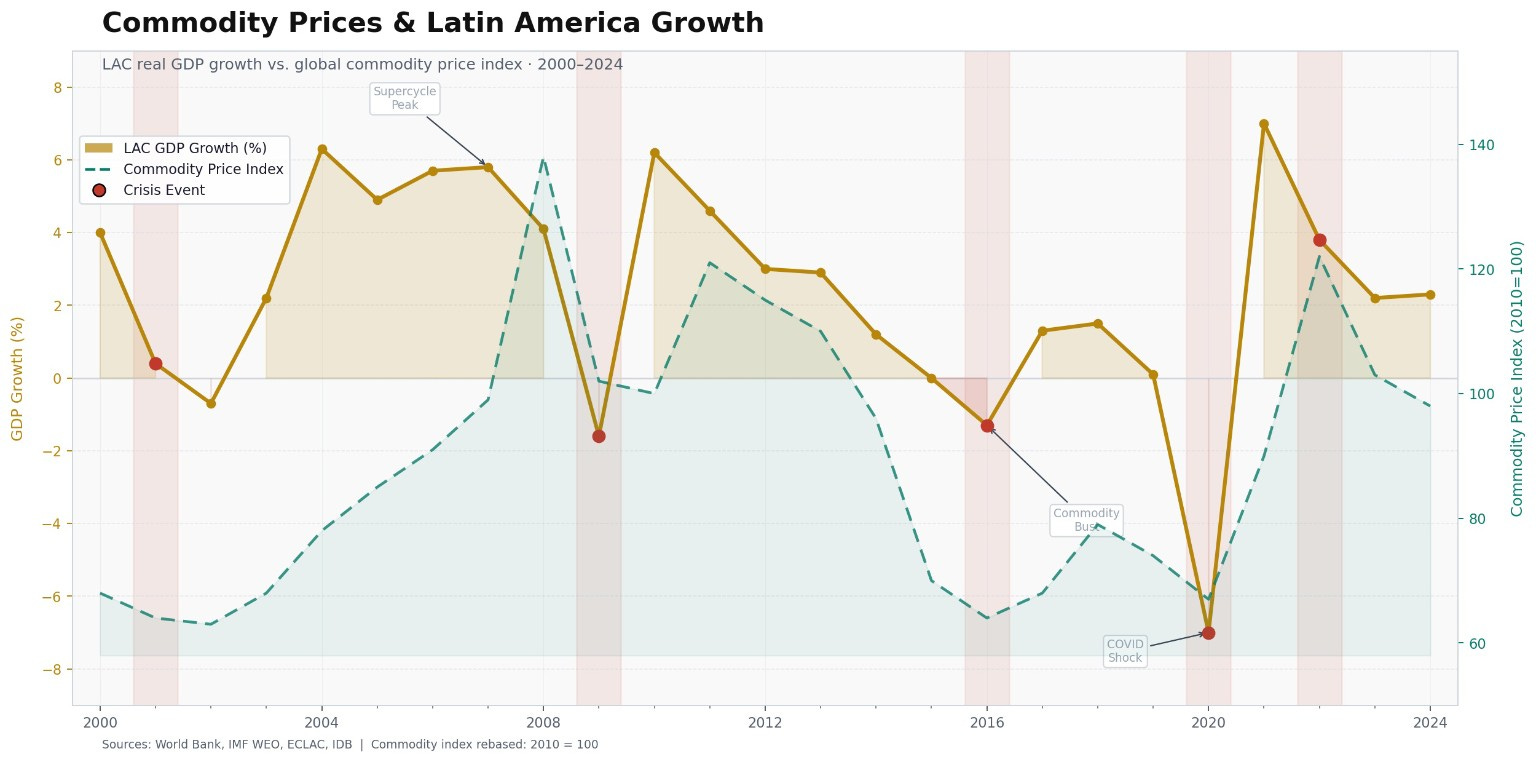

The appreciation of currencies and short term growth spurts driven by commodity cycles have historically failed to translate into broad based prosperity across the region. Industrial competitiveness remains weak, income inequality persists, and productivity growth has lagged behind other emerging regions, particularly Asia.

In many cases, the very forces that strengthen currencies in commodity booms has simultaneously undermine long term development by reinforcing dependence on natural resources and weakening manufacturing sectors through currency overvaluation.

This paradox is not new. It is deeply embedded in the economic history of Latin America.

Commodities are the centre piece to Understand the economies of Latin America

For much of its modern history, Latin Ameica has been integrated into the global economy primarily through the export of natural resources. While industrialization has expanded over the twentieth century, commodities continue to form the backbone of Latin America’s connection with the rest of the world.

A large share of Latin American exports still consists of primary products such as minerals, agricultural goods, and energy resources. Countries in the region often specialize in commodities that reflect their geography and natural endowments. Chile, for instance, is known for copper exports due to its vast mineral deposits, while Colombia historically built its export base around coffee. Argentina developed a strong position in meat and agricultural exports because of its fertile land and temperate climate.

Even in cases where manufactured exports appear significant, many of them are still closely tied to natural resources. Products such as textiles, leather goods, and furniture frequently rely on raw materials sourced locally. As a result, the export structure of Latin America remains fundamentally commodity driven.

In some cases, the export economy has also been influenced by illegal trade. Colombia offers a well-known example where narcotics exports have historically played a role in the economy. Estimates suggest that the value of drug exports has at times accounted for around a quarter of total exports and several percent of national output. While illegal, these activities illustrate how powerful export incentives can be in shaping economic structures.

However, the exploitation of natural resources has often come at a significant environmental cost. Across the region, forests have been depleted, rivers polluted, and ecosystems damaged by unregulated extraction. The environmental challenge is particularly visible in the Amazon Basin, which stretches across several South American countries including Brazil, Peru, Colombia, Ecuador, and Venezuela. The Amazon contains the largest tropical rainforest in the world and plays a critical role in regulating the global climate.

The destruction of these forests has raised concerns about global warming and the greenhouse effect. As a result, Latin American governments increasingly face pressure from the international community to adopt stricter environmental standards. Balancing economic development with environmental protection remains one of the region’s most complex policy challenges.

Industrialisation in Latin America

While natural resources dominated early development, Latin America also experienced significant industrialization during the twentieth century. The process accelerated after the Great Depression of the 1930s and during the Second World War. During these periods, global trade disruptions limited the availability of imported manufactured goods. This forced many countries in the region to begin producing goods domestically.

Governments adopted policies that supported industrial growth, including tariffs and other barriers designed to protect local industries from foreign competition. This strategy, often referred to as import substitution industrialization, encouraged the development of domestic manufacturing sectors. By the mid twentieth century, manufacturing had overtaken agriculture as a contributor to national output in several Latin American economies.

Industrial growth was rapid, but it was not always efficient. Many firms operated in protected markets where competition was limited. Shielded by high tariffs, companies often produced goods that were relatively expensive and of lower quality compared with international standards. As a result, many Latin American industries struggled to compete in global markets.

This structural weakness created a continuing dependence on commodity exports.

Even as manufacturing expanded domestically, foreign exchange earnings still largely came from the sale of primary products. These earnings were needed to finance imports and to service external debt.

The vulnerability of this model became clear during the debt crisis of the 1980s. In the 1970s, many Latin American governments borrowed heavily from international lenders, partly in response to global economic shocks such as the oil crises. When global interest rates rose and commodity prices weakened, countries across the region found it increasingly difficult to repay their debts.

The crisis forced a reassessment of economic policies. Governments began to focus more on improving efficiency, reducing trade barriers, and encouraging industries to become internationally competitive.

Foreign investment has also played a significant role in shaping the region’s development. During the nineteenth century, Great Britain was the dominant investor in Latin America, financing railways, mining operations, and infrastructure projects. By the early twentieth century, the United States had largely replaced Britain as the primary source of foreign capital.

Over time, many governments expanded the role of the state in economic activity. Public utilities, railways, and natural resource industries were often brought under government control. State participation in the economy became particularly strong during the 1960s and 1970s.

Despite these efforts, Latin America continues to face severe income inequality.

The roots of this inequality can be traced back to colonial land ownership patterns, where land and wealth were concentrated in the hands of a small elite. Industrial and financial concentration during the twentieth century reinforced this pattern, leaving the region with some of the most unequal income distributions in the world.

Understanding Latin America’s development also requires recognizing the concept sometimes described as the “commodity lottery.” Countries do not choose their natural resource endowments. Instead, geography and geology determine which commodities they can produce. These differences influence economic opportunities and long term growth trajectories.

Some commodities generate strong linkages with other sectors of the economy. For example, livestock production may stimulate industries related to processing, transportation, and equipment. Other commodities, however, offer fewer opportunities for broader development.

Productivity Gains of Commodities exports is concentrated

Ultimately, the success of an export based economy depends on how effectively productivity gains in the export sector spread to the rest of the economy. When the mechanisms of capital investment, labor development, and state policy function well, export growth can raise living standards and promote long-term economic expansion. When these mechanisms fail, growth remains concentrated in the export sector, leaving the broader economy vulnerable to fluctuations in global markets.

For Latin America, this tension between resource wealth and economic diversification continues to shape its development path.

In the end, the strength of Latin American currencies often reflects the strength of commodities rather than the strength of underlying economies.

Periods of currency appreciation are frequently driven by rising oil, metals, and agricultural prices, supported by capital inflows seeking yield due to higher interest rates . Yet these gains are largely cyclical, tied to external demand and global price movements rather than domestic productivity or industrial depth.

Until the link between export gains and domestic productivity is strengthened, Latin America’s currencies may continue to behave like winners, even as its economies remain constrained by the same structural limitations.

( Notes ~ The Economic History of Latin America since Independence by Victor Bulmer - Thomas)